Advice

Why Self-Employed Borrowers Get Told “No” Even When They Make Good Money

Self-employed borrowers can earn strong income and still face mortgage challenges. Learn why the right structure and strategy can make all the difference.

Self-employed borrowers can earn strong income and still face mortgage challenges. Learn why the right structure and strategy can make all the difference.

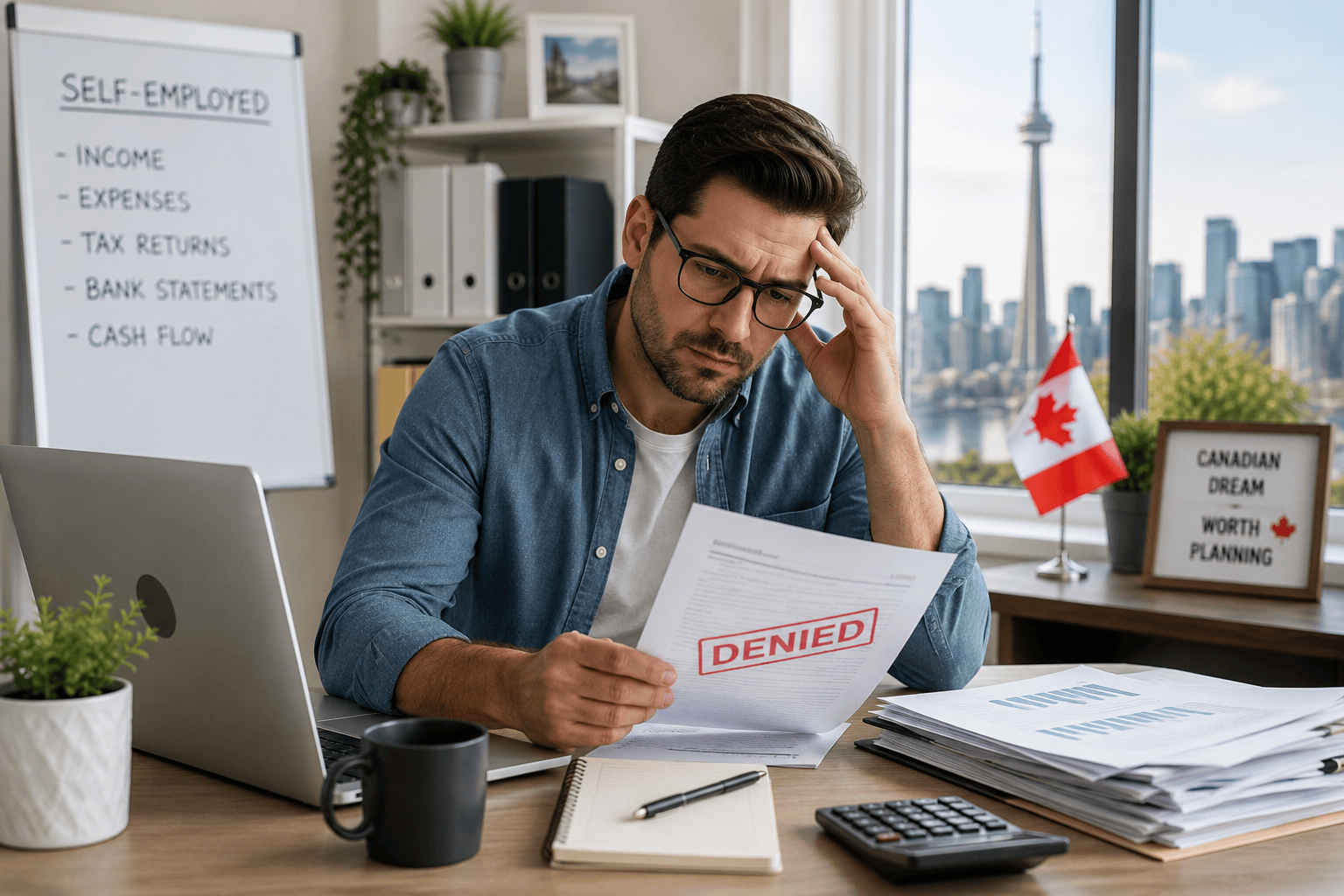

One of the most frustrating things about being self-employed is that making good money does not always mean getting an easy mortgage approval.

That sounds backwards, but it happens all the time.

A business owner can have strong income, valuable real estate, years of experience, and a perfect payment history — and still get declined by a bank.

Not because they cannot afford the mortgage.

It’s because their file does not fit neatly into the bank’s standard box.

I recently spoke with a business owner who had been put through the ringer.

He had multiple moving parts in his financial life. Business income. Corporate documents. Personal credit being used for business expenses. Strong equity in his properties. A mortgage coming up for renewal. And a credit report that did not fully reflect the reality of how money was moving through his business.

On paper, parts of the file looked messy.

But once you actually understood the full picture, the situation made a lot more sense.

That is the challenge many self-employed Canadians face.

Banks often look at one piece of the file and make a decision before understanding the whole story.

They may see high credit card utilization, but not realize the card is being used heavily for business purchases and paid down constantly.

They might see personal debt, but not understand that some of that debt is really connected to the business.

Inexperienced “corporate employee eyes” look at tax documents for an entrepreneur and not understand how the business actually generates income.

They fail to see the overall strength of the borrower.

For a self-employed person, that can be incredibly frustrating.

A salaried employee usually has a much simpler mortgage application.

They provide a job letter, a pay stub, and maybe a T4. The lender can quickly see their income and make a decision.

Self-employed borrowers are different.

Their income may come through a corporation. They may pay themselves by salary, dividends, or a combination of both. Their business may retain profit. Their accountant may structure things in a way that is tax-efficient, but not always mortgage-friendly.

That does not mean the income is not real.

It just means it needs to be explained properly.

This is where many mortgage applications fall apart.

A lender may not take the time to understand the business. A broker may not know which lender is best suited for that type of file. Or the application may be submitted without the right supporting documents and story behind the numbers.

When that happens, the borrower hears the same thing over and over again:

“Sorry, we can’t do it.”

But sometimes the real answer is: “We don’t understand it.”

With self-employed mortgage files, the way the deal is structured can make a massive difference.

It is about asking better questions.

What does the business actually earn?

How is the borrower paying themselves?

Are there retained earnings inside the corporation?

What debt is personal versus business-related?

What does the credit report show, and does it tell the full story?

Is there equity available in a property that could improve cash flow or clean up the file?

Is the goal to solve the immediate mortgage problem, or to build a better long-term lending profile?

These questions matter because self-employed borrowers often need more than a quick approval.

They need a strategy.

Sometimes the best solution is to

- move the mortgage to a lender that understands business owners.

- create more liquidity.

- fix the way the file appears on paper so that, six to twelve months later, the borrower is in a stronger position with major banks.

The right solution depends on the full picture.

One of the biggest mistakes self-employed borrowers make is assuming that one bank’s “no” means every lender will say no.

That is not always true.

Different lenders look at self-employed income differently. Some care more about declared income. Some will review corporate financials. Some are more flexible with business-for-self clients. Some understand retained earnings, add-backs, or alternative documentation better than others.

The key is knowing where the file fits before sending it everywhere.

That is important because every unnecessary application can create more stress, more delays, and sometimes more credit inquiries.

A complicated file should not be thrown at random lenders hoping one of them says yes.

It should be reviewed, structured, and positioned carefully.

For many self-employed clients, the immediate goal is obvious.

They need the mortgage done.

They have a renewal coming up. They want to refinance. They need to access equity. Or they are trying to purchase a property.

But the bigger goal should be to make sure they are not stuck in the same stressful position again next year.

That is where planning matters.

A good mortgage strategy should look beyond the closing date. It should consider how the borrower can improve their lending profile, reduce unnecessary stress, and create better options in the future.

For a self-employed person, that might mean improving how business expenses flow. It might mean restructuring debt. It might mean increasing liquidity. It might mean preparing documents earlier. It might mean working with the accountant and mortgage advisor together so the tax strategy and mortgage strategy are not fighting each other.

Because for business owners, the mortgage is rarely just about the mortgage.

It is connected to cash flow, taxes, credit, business structure, and long-term planning.

If you are self-employed and you have been told no by the bank, it does not automatically mean your situation cannot be fixed.

It may mean your file needs to be understood properly.

Self-employed borrowers often have more options than they realize.

The key is working with someone who knows how to look at the entire picture — not just one number on a credit report.

If your mortgage renewal, refinance, or purchase feels more complicated than it should, reach out. We can review the situation, look at the numbers, and help you understand what options may be available.

When planning to buy a new house, choose our Mortgage Team which has many professionals who look out for your best interest.

Contact Us Today

Kanga Mortgage provides services to clients across Ontario

Ajax | Aurora | Peterborough | Barrie | Bowmanville | Brampton | Brantford | Burlington | Cambridge | Chatham | Clarington | Cooksville | Durham Region | Etobicoke | GTA | Guelph | Halton Region | Hamilton | Kawartha | Kingston | Kitchener | London | Markham | Milton | Mississauga | Muskoka | Newmarket | Niagara | North York | Oakville | Oshawa | Ottawa | Peel Region | Pickering | Richmond Hill | Sault Ste Marie | Scarborough | Saint Catharines | Seaton | Stouffville | Sudbury | Thornhill | Thunder Bay | Toronto | Unionville | Uxbridge | Vaughan | Waterloo | Whitby | Windsor | York

.svg)